What to do if your insurance company denies a storm damage claim 2026

Table of Contents

- Understanding Your Insurance Policy

- Common Reasons for Claim Denial

- Steps to Take After a Claim Denial

- How to Appeal a Denied Claim

- Seeking Professional Help

Understanding Your Insurance Policy

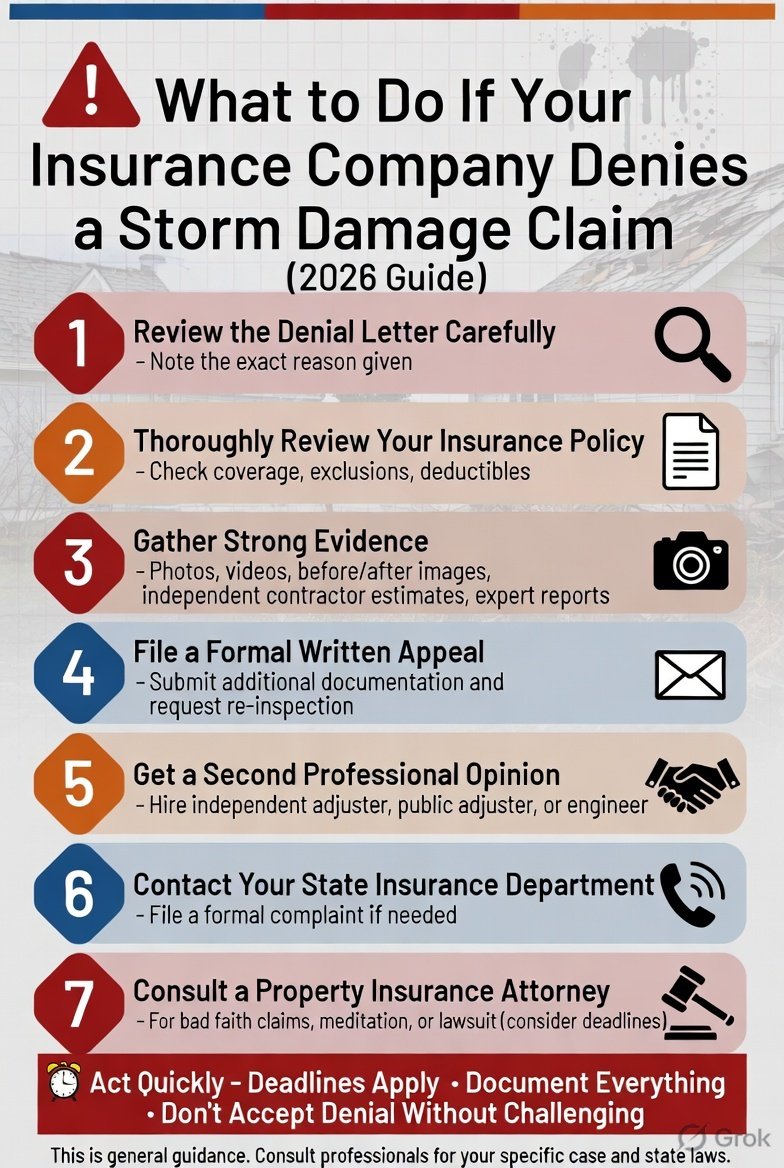

Before diving into the process of appealing a denied claim, it's essential to understand your insurance policy. Review your policy documents to know what is covered and what is not. Check for any exclusions, limitations, or deductibles that may apply to your situation. Knowing your policy inside out will help you identify any potential weaknesses in the insurer's denial reasoning.

For instance, if you have a homeowner's insurance policy, check if it covers storm damage, including wind and flood damage. Some policies may have separate deductibles for different types of damage, so it's crucial to understand these details. Additionally, review your policy's requirements for filing a claim, including any deadlines or documentation needed.

Common Reasons for Claim Denial

Insurance companies often deny claims due to various reasons, including insufficient documentation, disputes over the cause of damage, or failure to meet policy requirements. Insurers may argue that the damage was not caused by the storm or that the policyholder did not provide adequate proof of the damage. In some cases, insurers may deny claims due to pre-existing conditions or maintenance issues.

For example, if you file a claim for roof damage after a storm, the insurer may deny it if they believe the damage was caused by wear and tear or poor maintenance rather than the storm itself. Similarly, if you fail to provide detailed documentation, such as photos or videos, the insurer may deny your claim due to lack of evidence.

Steps to Take After a Claim Denial

If your insurance company denies your storm damage claim, don't panic. There are steps you can take to appeal the decision and potentially overturn it. First, review the denial letter carefully to understand the reasons for the denial. Check if the insurer has provided any evidence to support their decision and if they have offered any alternatives or next steps.

Next, gather any additional evidence that may support your claim, such as repair estimates, photos, or witness statements. You can also contact your insurer to request a re-evaluation of your claim or to provide additional information. Keep a record of all correspondence with your insurer, including dates, times, and details of conversations.

How to Appeal a Denied Claim

If you believe your insurer has unfairly denied your claim, you can appeal the decision. Start by reviewing your policy to understand the appeals process and any deadlines that may apply. You can then submit a written appeal to your insurer, providing any additional evidence or information that supports your claim.

Be sure to include any relevant documentation, such as receipts, invoices, or expert opinions. You can also request a meeting with your insurer to discuss your appeal and provide additional context. If your insurer still denies your appeal, you may need to seek external help, such as consulting with a public adjuster or seeking legal advice.

Seeking Professional Help

If you're struggling to navigate the claims process or need help appealing a denied claim, consider seeking professional help. A public adjuster can help you negotiate with your insurer and ensure you receive a fair settlement. They can also help you understand your policy and identify any potential weaknesses in the insurer's denial reasoning.

Alternatively, you can seek legal advice from an attorney specializing in insurance law. They can help you understand your rights and options and represent you in any disputes with your insurer. Remember, you have the right to fair treatment and a reasonable settlement, so don't be afraid to seek help if you need it.

What are my rights if my insurance company denies my storm damage claim?

If your insurance company denies your storm damage claim, you have the right to appeal the decision. You can start by reviewing your policy to understand the appeals process and any deadlines that may apply. You can then submit a written appeal to your insurer, providing any additional evidence or information that supports your claim.

You also have the right to seek external help, such as consulting with a public adjuster or seeking legal advice. A public adjuster can help you negotiate with your insurer and ensure you receive a fair settlement, while an attorney can help you understand your rights and options and represent you in any disputes with your insurer.

How long do I have to appeal a denied storm damage claim?

The time limit for appealing a denied storm damage claim varies depending on your insurance policy and state laws. Typically, you have between 30 to 60 days to appeal a denied claim, but this can range from 15 to 180 days in some cases. It's essential to review your policy and understand the appeals process to ensure you don't miss any deadlines.

Additionally, some states have specific laws governing the appeals process, so it's crucial to familiarize yourself with these laws and regulations. If you're unsure about the appeals process or need help navigating it, consider seeking professional help from a public adjuster or attorney.

Can I sue my insurance company if they deny my storm damage claim?

If your insurance company denies your storm damage claim and you believe they have acted in bad faith, you may be able to sue them. Bad faith refers to any unfair or deceptive practices by the insurer, such as denying a claim without a reasonable basis or failing to investigate a claim properly.

To sue your insurance company, you'll need to provide evidence of bad faith and demonstrate that you've suffered damages as a result. This can include any financial losses, emotional distress, or other harm caused by the insurer's actions. It's essential to seek legal advice from an attorney specializing in insurance law to understand your rights and options.

How can I prevent my insurance company from denying my storm damage claim?

To prevent your insurance company from denying your storm damage claim, it's essential to understand your policy and the claims process. Review your policy to know what is covered and what is not, and check for any exclusions, limitations, or deductibles that may apply to your situation.

Additionally, keep detailed records of any damage, including photos, videos, and repair estimates. Provide your insurer with any requested documentation, and respond promptly to any inquiries or requests. It's also crucial to maintain your property and keep it in good condition to reduce the risk of damage and potential denials.

What are some common mistakes to avoid when filing a storm damage claim?

When filing a storm damage claim, there are several common mistakes to avoid. These include failing to review your policy, not providing adequate documentation, and not responding promptly to insurer requests. Additionally, be cautious of any delays or lack of communication from your insurer, as these can be signs of bad faith.

It's also essential to avoid accepting a low settlement offer without fully understanding the terms and conditions. If you're unsure about any aspect of the claims process, consider seeking professional help from a public adjuster or attorney to ensure you receive a fair settlement.

How can I get help with my storm damage claim?

If you need help with your storm damage claim, there are several options available. You can start by contacting your insurer to request assistance or guidance. If you're not satisfied with their response, consider seeking professional help from a public adjuster or attorney.

A public adjuster can help you navigate the claims process, ensure you receive a fair settlement, and provide expert advice on any disputes with your insurer. An attorney can help you understand your rights and options, represent you in any disputes, and provide guidance on any legal matters related to your claim.

Frequently Asked Questions

What are my rights if my insurance company denies my storm damage claim?

If your insurance company denies your storm damage claim, you have the right to appeal the decision. You can start by reviewing your policy to understand the appeals process and any deadlines that may apply. You can then submit a written appeal to your insurer, providing any additional evidence or information that supports your claim.

How long do I have to appeal a denied storm damage claim?

The time limit for appealing a denied storm damage claim varies depending on your insurance policy and state laws. Typically, you have between 30 to 60 days to appeal a denied claim, but this can range from 15 to 180 days in some cases. It's essential to review your policy and understand the appeals process to ensure you don't miss any deadlines.

Can I sue my insurance company if they deny my storm damage claim?

If your insurance company denies your storm damage claim and you believe they have acted in bad faith, you may be able to sue them. Bad faith refers to any unfair or deceptive practices by the insurer, such as denying a claim without a reasonable basis or failing to investigate a claim properly.

How can I prevent my insurance company from denying my storm damage claim?

To prevent your insurance company from denying your storm damage claim, it's essential to understand your policy and the claims process. Review your policy to know what is covered and what is not, and check for any exclusions, limitations, or deductibles that may apply to your situation.

What are some common mistakes to avoid when filing a storm damage claim?

When filing a storm damage claim, there are several common mistakes to avoid. These include failing to review your policy, not providing adequate documentation, and not responding promptly to insurer requests. Additionally, be cautious of any delays or lack of communication from your insurer, as these can be signs of bad faith.

How can I get help with my storm damage claim?

If you need help with your storm damage claim, there are several options available. You can start by contacting your insurer to request assistance or guidance. If you're not satisfied with their response, consider seeking professional help from a public adjuster or attorney.

, Coding & Data Science Education Guide in India")